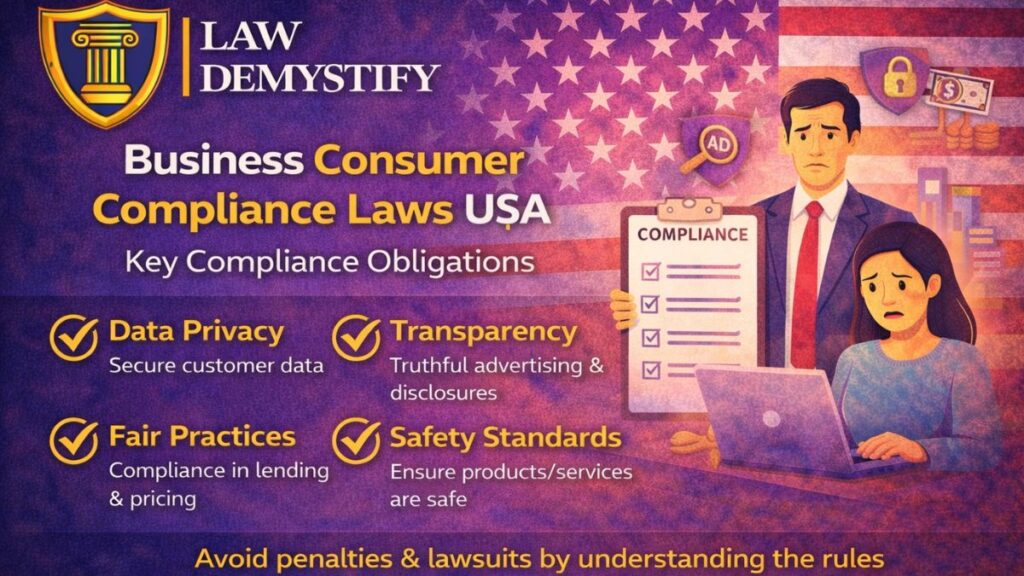

In the United States, consumer protection is not optional or aspirational—it is a binding legal obligation. Businesses that offer goods, services, housing, or financial products operate under rules that directly affect how they advertise, bill, and interact with customers. From large corporations and banks to local landlords and property managers, businesses operate within a regulatory framework designed to ensure fairness, transparency, and accountability. This framework is commonly described as business consumer compliance laws USA, and it shapes how companies interact with consumers at every stage of a transaction.

For tenants and landlords, these laws often intersect with everyday housing and rental practices—such as how rent is collected, how fees are described, and how disputes are handled when something goes wrong.

This guide explains how business consumer compliance laws USA function at both the federal and state levels, how they apply to housing-related businesses, and what happens when companies fail to comply. It is written for educational purposes only and focuses on explaining legal standards rather than offering advice or predicting outcomes.

These obligations exist alongside broader consumer rights USA protections that govern how individuals can dispute charges, report unfair practices, and seek correction when businesses fail to comply.

The Purpose and Scope of Business Consumer Compliance Laws

At their core, business consumer compliance laws USA exist to correct power imbalances between businesses and individual consumers. Companies typically control pricing, contract terms, billing systems, and information flow, while consumers often must accept standard terms to secure housing, credit, or essential services.

Consumer protection law addresses this imbalance by requiring businesses to follow basic standards of fairness, including duties to:

- Act honestly and transparently

- Avoid deceptive or unfair practices

- Honor advertised terms and written agreements

- Provide clear dispute and refund processes

These obligations apply regardless of whether the business intends to harm consumers. Even unintentional violations can trigger enforcement if legal standards are not met.

Federal Authority Governing Consumer Compliance

Federal consumer protection law establishes nationwide minimum standards. These laws apply across all states and are enforced by federal agencies. Businesses operating in housing-related markets—such as landlords accepting electronic rent payments or property managers charging service fees—are often subject to these federal rules.

Key federal statutes underlying business consumer compliance laws USA include laws regulating billing accuracy, disclosures, debt collection, and unfair practices. While these statutes differ in scope, they share common principles: consumers must receive accurate information, fair treatment, and meaningful remedies when errors or misconduct occur.

Federal law generally preempts weaker state rules but allows states to enact stronger protections. This layered structure ensures a consistent baseline while permitting states to respond to local conditions.

The Role of Federal Enforcement Agencies

Several agencies oversee compliance with federal consumer protection standards. The Consumer Financial Protection Bureau focuses on financial products and services, including payment systems, credit reporting, and debt collection. The Federal Trade Commission addresses unfair or deceptive acts across a broad range of industries.

For housing-related businesses, federal oversight often arises when financial transactions are involved—especially when consumers report billing errors, misleading fees, or unresolved payment disputes. For example, a landlord who uses an online platform to process rent payments may fall under federal scrutiny if fees are misleading or billing errors are mishandled. In such cases, consumer protection compliance for businesses is not limited to traditional lenders—it extends to any company engaging in covered conduct.

State Consumer Protection Laws and Business Obligations

While federal law sets the floor, state law often defines the ceiling. Every state has its own consumer protection statute, many of which impose additional duties on businesses. These laws frequently apply to rental housing transactions, including advertising, fee disclosures, and refund practices.

State statutes typically prohibit unfair or deceptive acts in trade or commerce. Although wording varies, courts generally interpret these laws broadly to protect consumers. For businesses, this means compliance is not one-size-fits-all. Practices that are acceptable in one state may violate consumer protection standards in another.

For example, some states require clearer disclosure of nonrefundable fees in rental agreements. Others impose strict timelines for refunds or prohibit certain charges altogether. These differences illustrate why business consumer compliance laws USA must be evaluated through both federal and state lenses.

How Consumer Protection Law Applies to Landlords and Property Managers

Landlords and property managers are treated as businesses under consumer law when they rent housing to the public—even if they view themselves primarily as housing providers rather than commercial operators. This classification triggers consumer protection compliance for businesses, even though housing law also governs many aspects of the landlord-tenant relationship.

Common areas where consumer protection duties arise include:

- Rental advertising and listings

- Application and screening fees

- Rent payment methods and service charges

- Utility billing and pass-through fees

Misrepresenting unit features, failing to disclose mandatory fees, or charging amounts inconsistent with advertised terms can expose landlords to liability under unfair business practices laws USA. These consumer compliance duties operate alongside tenant rights USA protections, which govern habitability standards, lease enforcement, and housing-related disclosures.

Advertising Standards and Deceptive Trade Practices

Advertising is often the first point of contact between a business and a consumer. U.S. law requires advertisements to be truthful and not misleading. This principle applies to online listings, printed materials, and verbal representations.

Under deceptive trade practices explained by courts and regulators, an advertisement can be unlawful if it omits material information or creates a misleading impression, even when the omission is unintentional. For example, advertising a low monthly rent while failing to disclose mandatory technology or service fees may violate consumer protection standards.

In housing contexts, deceptive advertising can occur when listings exaggerate amenities, misstate lease terms, or conceal required charges. Businesses must ensure that marketing materials align with actual contractual obligations to satisfy business consumer compliance laws USA.

Fee Disclosures and Transparency Requirements

Transparency is a recurring theme in consumer protection law. Businesses must clearly disclose fees before consumers are legally obligated to pay them. This requirement is especially relevant in rental housing, where application fees, convenience fees, and service charges are common.

Failure to disclose fees upfront may constitute an unfair or deceptive practice. Even if a fee is permissible under housing law, it may still violate consumer protection compliance for businesses if disclosure is inadequate.

Courts often examine whether a reasonable consumer would have understood the true cost of the transaction at the time of agreement—not after fees appeared on a statement. If not, the business may be held accountable under unfair business practices laws usa.

Billing Accuracy and Error Resolution Duties

Once a transaction begins, businesses must maintain accurate billing systems. Federal and state laws impose duties to investigate and correct billing errors when consumers raise disputes.

In rental scenarios, billing disputes may involve incorrect rent amounts, duplicate charges, or misapplied payments. When a tenant notifies a landlord or property manager of an error, the business must respond according to applicable procedures. Ignoring disputes or placing the burden entirely on the consumer—such as requiring repeated follow-ups without any meaningful investigation—can violate business consumer compliance laws USA.

Error resolution obligations are particularly strict when electronic payments or third-party processors are involved. Businesses remain responsible for compliance even when vendors handle transactions on their behalf.

Refund Policies and Legal Requirements

Refund practices are a frequent source of consumer disputes. While businesses are not always required to offer refunds, when they do, the terms must be clearly stated and honored. Misrepresenting refund eligibility or imposing undisclosed conditions after payment may violate refund policy legal requirements usa and lead to enforcement action.

In housing-related transactions, refunds often involve application fees, security deposits, or overpayments. State laws commonly regulate security deposit refunds, but consumer protection law governs how refund policies are communicated and enforced.

For example, advertising an application fee as refundable when it is not—or delaying refunds beyond stated timelines—can expose a business to enforcement under consumer protection compliance for businesses.

Unfair Practices and Substantive Fairness

Not all violations involve deception. Some practices are deemed unfair because they cause substantial consumer harm that is not reasonably avoidable. Courts and regulators evaluate unfairness by examining the real-world impact on consumers.

Examples in housing-related businesses may include:

- Imposing excessive convenience fees with no meaningful alternative

- Structuring payment systems to generate predictable penalties

- Exploiting information asymmetry to shift costs to tenants

These practices may violate unfair business practices laws USA even if disclosures exist. The law focuses on substance, not just form.

State-by-State Variations in Enforcement and Remedies

Consumer protection enforcement varies significantly by state. Some states allow consumers to sue for statutory damages without proving actual loss. Others permit recovery of attorney’s fees, making enforcement more accessible.

Timelines also differ. For instance, statutes of limitations for consumer claims may range from one to four years depending on the state. Housing-related businesses operating in multiple jurisdictions must tailor compliance programs accordingly to satisfy business consumer compliance laws USA across state lines.

State attorneys general play a major role in enforcement. They may bring actions against businesses engaged in widespread violations, including property management companies with systemic billing issues.

Interaction Between Housing Law and Consumer Protection Law

Housing law and consumer protection law operate in parallel. Compliance with landlord-tenant statutes does not automatically ensure compliance with consumer law. A fee permitted under housing regulations may still be unlawful if disclosed improperly or applied unfairly.

For example, a state housing code may allow certain administrative fees, but consumer protection law may require clearer disclosure or prohibit deceptive marketing. Businesses must evaluate obligations holistically rather than relying on a single legal framework.

This interaction underscores why business consumer compliance laws USA are particularly important for landlords and housing providers.

Common Compliance Mistakes Businesses Make

Many consumer law violations do not arise from intentional misconduct but from routine operational mistakes. In housing-related businesses, common compliance failures include relying on outdated lease templates, copying fee language from third-party platforms, or assuming that practices allowed in one state automatically apply elsewhere.

Another frequent issue is failing to update disclosures when billing systems or payment processors change. Even small changes—such as adding a convenience fee or switching rent platforms—can trigger new disclosure obligations under business consumer compliance laws USA.

Real-World Example: Rent Payment Platform Fee Dispute

In several enforcement actions and consumer complaints, property managers have faced scrutiny after using third-party rent payment platforms that added mandatory convenience fees without clear disclosure. Even when the platform processed payments correctly, businesses remained responsible for explaining fees upfront and resolving billing disputes when tenants raised concerns.

These situations illustrate how business consumer compliance laws USA apply even when billing systems are outsourced to external vendors.

Consequences of Non-Compliance for Businesses

Violating consumer protection laws can lead to multiple consequences. These may include government enforcement actions, monetary penalties, restitution orders, and injunctive relief requiring changes in business practices.

In some cases, private lawsuits may also arise. While outcomes vary, the risk of enforcement incentivizes businesses to maintain robust compliance systems. Ignorance of the law is not a defense under consumer protection compliance for businesses.

Beyond legal consequences, non-compliance can damage reputation and consumer trust—critical factors in competitive housing markets.

The Importance of Compliance Systems and Training

Effective compliance requires more than written policies. Businesses must train staff, monitor practices, and respond promptly to consumer concerns. In housing-related businesses, frontline employees often interact directly with tenants, making training especially important.

Compliance systems should address advertising, fee disclosures, billing accuracy, and dispute resolution. Regular audits help identify risks before they escalate into violations of business consumer compliance laws USA.

Compliance vs Best Practices in Consumer Protection

Legal compliance sets the minimum standard businesses must meet. Best practices go further by reducing disputes before they arise. For example, while the law may require disclosure of fees, best practices include explaining those fees in plain language and offering accessible support when questions arise.

Businesses that treat compliance as a checklist often face recurring disputes. Those that treat it as an operational principle tend to build stronger tenant and customer relationships over time.

When Businesses Should Seek Legal Guidance

Not every consumer issue requires legal intervention. However, businesses should consider seeking professional guidance when facing repeated billing complaints, regulatory inquiries, or operating across multiple states with different consumer protection standards.

Early legal review often prevents small compliance gaps from turning into costly enforcement actions under business consumer compliance laws USA.

Frequently Asked Questions

What laws must businesses follow to protect consumers?

Businesses must comply with federal and state consumer protection statutes that prohibit unfair or deceptive practices and require transparency under business consumer compliance laws USA.

What is illegal for a business to do to customers?

Misleading advertising, hidden fees, unfair billing practices, and deceptive refund policies may violate unfair business practices laws usa.

What happens if a business violates consumer law?

Consequences may include government enforcement, penalties, restitution, or court-ordered changes in practices under consumer protection compliance for businesses.

Do consumer protection laws apply to landlords?

Yes. When landlords engage in commerce, they are subject to business consumer compliance laws USA alongside housing regulations.

Are refund policies regulated by law?

Refund terms must be accurately disclosed and honored under refund policy legal requirements usa when offered.

Can state law be stricter than federal law?

Yes. States may impose stronger protections and remedies in addition to federal standards.

Do honest mistakes still count as violations?

Intent is not always required. Practices that meet statutory definitions of unfairness or deception may violate business consumer compliance laws USA even without intent.

The Ongoing Role of Consumer Compliance in Housing and Commerce

Consumer protection law continues to evolve as markets and technologies change. Digital payment systems, automated billing, and online leasing platforms introduce new compliance challenges. Regulators increasingly scrutinize these systems to ensure that consumer protections keep pace with innovation.

For businesses operating in housing and related sectors, understanding and respecting business consumer compliance laws USA is not merely a regulatory obligation—it is a fundamental component of lawful, sustainable operations. By adhering to transparency, fairness, and accountability, businesses align their practices with both legal requirements and consumer expectations, reinforcing trust in the marketplace.

Helpful