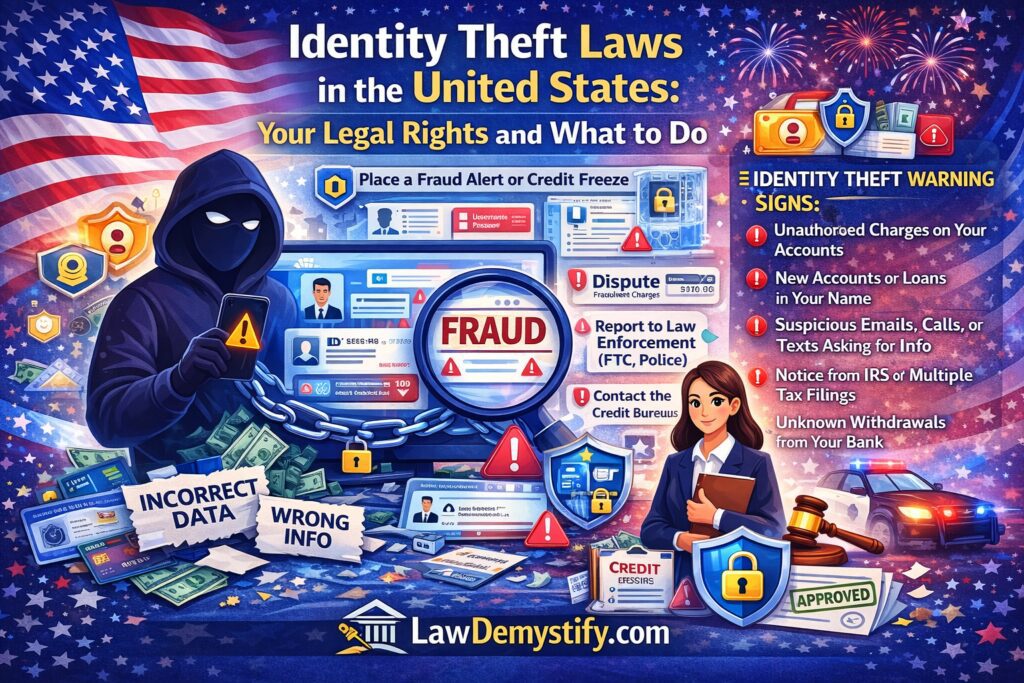

Identity theft is no longer a rare or isolated crime. It affects millions of Americans each year and increasingly intersects with housing, rental applications, utilities, employment, and consumer credit. For tenants and landlords alike, identity theft can trigger denied housing, unlawful collections, damaged credit, and long-term financial consequences if not addressed properly and lawfully.

In real life, many victims do not realize identity theft has occurred until a housing application is denied or a collection notice appears for a property they never lived in. By the time the mistake is discovered, the damage to credit or housing options may already be underway.

This guide explains identity theft laws usa in clear, practical terms. It walks through how identity theft is defined under U.S. law, which federal and state authorities regulate it, how housing-related identity theft commonly occurs, and the legal steps after identity theft that victims are entitled to take. The focus is education—not legal advice—designed to help consumers, tenants, and property owners understand their rights and obligations under U.S. law.

Understanding Identity Theft Under U.S. Law

Identity theft occurs when someone uses another person’s personal identifying information—such as a Social Security number, date of birth, driver’s license number, or financial account data—without authorization, usually for financial gain. Under identity theft laws usa, this conduct is regulated at both the federal and state levels, with overlapping but distinct enforcement systems.

From a housing perspective, identity theft often shows up when a tenant discovers:

- A rental application was submitted using their information

- A lease or utility account was opened in their name

- Collections appear for unpaid rent at a property they never lived in

- A background or credit check reflects fraudulent activity

Understanding how the law defines identity theft is the first step in protecting identity theft victim rights.

In practice, identity theft is rarely discovered through alerts or warnings. More often, it surfaces during routine life events such as applying for housing, utilities, or employment background checks.

Federal Identity Theft Law Framework

At the federal level, identity theft is primarily governed through criminal statutes and consumer protection laws. These laws establish baseline rights for victims and compliance obligations for businesses, including landlords and property managers.

Identity Theft and Assumption Deterrence Act

This federal statute criminalizes the knowing transfer, possession, or use of another person’s means of identification with unlawful intent. While enforcement is handled by federal prosecutors, the law forms the backbone of identity theft laws usa by defining identity theft as a standalone offense.

Fair Credit Reporting Act (FCRA)

The FCRA plays a central role in identity theft recovery. It regulates how credit reporting agencies, landlords, screening companies, and creditors handle consumer information. Under the FCRA, identity theft victims have the right to:

- Dispute inaccurate or fraudulent credit information

- Place fraud alerts and credit freezes

- Receive documentation used in fraudulent transactions

When a tenant is denied housing due to fraudulent credit data, the FCRA becomes one of the most important legal tools in the identity theft reporting process.

Fair and Accurate Credit Transactions Act (FACTA)

FACTA amended the FCRA to expand protections for identity theft victims. It introduced mandatory identity theft reports, free credit reports, and stronger obligations on businesses to prevent misuse of consumer data.

Together, these federal laws establish nationwide minimum standards. States are allowed to expand—but not reduce—these protections.

State Identity Theft Laws and Enforcement Differences

While federal law creates uniform baseline protections, state identity theft laws vary significantly in scope, remedies, and timelines. Every state criminalizes identity theft, but civil remedies and consumer rights differ.

Key State-Level Variations

State laws may differ in:

- How quickly fraud alerts or credit freezes must be processed

- Whether victims can sue for statutory damages

- How long creditors must investigate disputes

- Whether landlords are required to provide application records

For example, some states impose strict deadlines on landlords to respond to identity theft claims involving rental applications, while others rely more heavily on federal FCRA timelines.

Understanding these differences is critical when navigating legal steps after identity theft, especially for tenants facing housing denials or eviction actions tied to fraud.

How Identity Theft Commonly Affects Tenants and Housing

In housing situations, identity theft often remains hidden until a tenant applies for a new apartment, renews a lease, or suddenly receives a collection notice tied to a property they never occupied.

Common Housing-Related Identity Theft Scenarios

- A fraudulent rental application submitted using stolen personal data

- A lease signed electronically without the victim’s knowledge

- Utility accounts opened under a tenant’s name

- Rental debt sold to collections for a property the victim never occupied

In each situation, identity theft victim rights protect consumers from being held responsible for debts they did not create—but only if the correct legal process is followed.

Legal Responsibilities of Landlords and Property Managers

Landlords and property managers are not law enforcement agencies, but they are regulated entities under federal and state consumer protection laws. When identity theft intersects with housing, landlords must comply with strict legal standards.

Screening and Application Obligations

When landlords use consumer reports or third-party screening services, they must comply with the FCRA. This includes:

- Using information only for permissible purposes

- Providing adverse action notices when denying applications

- Responding to disputes involving fraudulent data

Failure to follow these rules may expose landlords to civil liability, even when the identity theft itself was committed by a third party.

Record Retention and Disclosure

In many states, landlords must retain rental application records for a defined period. When identity theft is alleged, victims may lawfully request copies of applications or lease documents used in the fraud as part of the identity theft reporting process.

Legal Steps After Identity Theft Is Discovered

For many people, discovering identity theft is overwhelming—especially when it disrupts housing, credit, or employment opportunities all at once. However, U.S. law follows a structured process. Taking the correct steps in the proper order is often more effective than reacting in panic.

Once identity theft is identified, timing matters. U.S. law gives victims powerful tools, but those tools must be used in the correct order to preserve legal rights and prevent further harm.

Initial Legal Recognition of Identity Theft

Under identity theft laws usa, identity theft is not legally recognized until it is formally reported. Informal complaints alone are not sufficient to trigger statutory protections.

The law generally requires:

- Documentation of the theft

- Notice to affected financial or housing entities

- Formal reporting through designated channels

These actions activate statutory duties owed to victims under federal and state law.

Identity Theft Reporting Process Explained

The identity theft reporting process is structured and sequential. While specific details vary by state, federal law provides a standardized framework.

Step One: Identity Theft Report

An identity theft report is a sworn statement asserting that personal identifying information was misused without authorization. This report becomes the foundation for enforcing identity theft victim rights.

In housing-related cases, this report may be used to:

- Remove fraudulent rental debt

- Block unlawful collections

- Correct tenant screening reports

Without this report, landlords and credit bureaus are not legally required to act.

Credit Reporting, Fraud Alerts, and Legal Protections

Credit reporting agencies play a central role in identity theft recovery. Federal law mandates specific protections once identity theft is properly documented.

Fraud Alerts Under Federal Law

A fraud alert warns creditors and landlords that identity theft may be involved and that additional verification is required before extending credit or approving housing.

Initial fraud alerts typically last one year, while extended alerts—available after confirmed identity theft—can last up to seven years under identity theft laws usa.

Credit Freeze Identity Theft Law Protections

A credit freeze restricts access to a consumer’s credit file entirely. Under credit freeze identity theft law, consumers are entitled to place and remove credit freezes at no cost.

For tenants, this can prevent future fraudulent rental applications or unauthorized utility accounts.

Credit Freeze and Housing Applications

This is a common real-world issue that can delay approvals even when the tenant has done everything else correctly, unless the credit freeze is temporarily lifted for tenant screening.

While a credit freeze protects against fraud, it can temporarily complicate legitimate housing applications. Landlords may be unable to access screening reports unless the tenant temporarily lifts the freeze.

Understanding how credit freeze identity theft law interacts with rental screening helps tenants avoid unnecessary delays while maintaining protection.

Identity Theft Fraud Recovery Steps in Housing Cases

Recovering from identity theft is rarely instant. The law recognizes this and provides structured remedies designed to restore victims to their pre-theft position.

Correcting Fraudulent Rental Records

When identity theft results in a false tenancy record, victims have the right to dispute that information with:

- Credit reporting agencies

- Tenant screening companies

- Collection agencies

- Landlords maintaining internal records

These identity theft fraud recovery steps must be completed in a specific sequence to ensure compliance obligations are triggered.

State-by-State Timelines and Enforcement Realities

While federal law provides uniform rights, enforcement timelines vary significantly by state.

Examples of State Differences

Some states require landlords to respond to identity theft documentation within 14 days. Others rely on federal 30-day investigation timelines. Certain states allow statutory damages for failure to correct records, while others limit remedies to actual losses.

These variations make understanding identity theft laws usa essential for tenants and landlords operating across state lines.

Lawful vs. Unlawful Practices After Identity Theft

Not every negative outcome following identity theft is unlawful. The distinction lies in whether regulated parties comply with statutory duties once notified.

Lawful Conduct

- Temporarily denying an application while verifying identity

- Requesting documentation consistent with federal law

- Pausing collection activity during investigation

Unlawful Conduct

- Continuing to collect a debt after receiving an identity theft report

- Refusing to correct proven fraudulent records

- Retaliating against a tenant asserting identity theft victim rights

Understanding these distinctions helps consumers identify when legal protections have been violated.

Tenant Remedies Under Identity Theft Laws

Tenants affected by identity theft are not powerless. The law provides multiple remedies depending on the nature of the harm.

Potential Remedies Include

- Removal of fraudulent debts

- Correction of tenant screening reports

- Damages for unlawful reporting or collection

- Injunctive relief to prevent ongoing harm

These remedies arise from compliance failures, not from the identity theft itself—a crucial distinction under identity theft laws usa.

Landlord and Business Compliance Obligations

Landlords are considered data users and, in some cases, data holders. This status carries legal responsibilities.

Compliance Duties After Notice

Once identity theft is reported, landlords must:

- Cease reliance on disputed fraudulent information

- Provide copies of application or lease documents used in fraud

- Cooperate with lawful investigations

Failure to do so may expose landlords to consumer protection claims, even if they were not responsible for the original theft.

Interaction Between Identity Theft and Eviction Proceedings

Identity theft can surface during eviction actions, particularly when unpaid rent is attributed to a tenant who never occupied the property.

In such cases, courts may require landlords to pause proceedings while identity theft claims are evaluated. Proper documentation is critical to preserving identity theft victim rights in housing court.

Long-Term Impact of Identity Theft on Housing Stability

Even after immediate disputes are resolved, identity theft can affect housing stability for years. Incorrect records may resurface, especially when data is resold or reused.

Understanding and completing all identity theft fraud recovery steps reduces the risk of future harm.

Preventive Legal Strategies for Tenants and Landlords

While no system is foolproof, lawful preventive measures reduce exposure.

Tenants benefit from monitoring reports, using fraud alerts strategically, and understanding credit freeze identity theft law options.

Landlords benefit from verifying identities consistently, securing application data, and responding promptly to disputes under the identity theft reporting process.

Frequently Asked Questions About Identity Theft Laws

What should a tenant do immediately after discovering identity theft?

The first step is to formally document the theft through the recognized reporting channels so legal protections under identity theft laws usa are activated. Without formal documentation, statutory rights may not apply.

Do you need a police report for identity theft to remove rental debt?

In many cases, a police report strengthens an identity theft claim, but federal law allows alternative identity theft reports to trigger identity theft victim rights, depending on the circumstances and state law.

How long does identity theft recovery take under U.S. law?

Recovery timelines vary based on the type of fraud and state enforcement rules. Some disputes resolve within weeks, while others involving housing records may take several months to fully correct. Housing-related identity theft cases often take longer because multiple parties—landlords, screening companies, and credit bureaus—may be involved.

Can a landlord deny a rental application due to suspected identity theft?

A landlord may pause or conditionally deny an application while verifying identity, but must comply with federal notice requirements and cannot rely on proven fraudulent data once notified.

Is a credit freeze required after identity theft involving housing?

A credit freeze is optional but strongly protected under credit freeze identity theft law. It can prevent future fraudulent rental applications but may need temporary lifting for legitimate housing checks.

Are tenants responsible for rent incurred through identity theft?

Tenants are not legally responsible for debts created through verified identity theft. Under identity theft laws usa, liability depends on compliance with reporting and dispute procedures.

Can identity theft affect future background or tenant screening reports?

Yes. If not fully corrected, fraudulent records may reappear. Completing all identity theft fraud recovery steps and monitoring reports helps prevent long-term housing consequences.

Educational Notice

This article is provided for general educational purposes only. It does not constitute legal advice, does not create an attorney-client relationship, and does not guarantee outcomes. Identity theft laws vary by jurisdiction, and individuals should seek qualified legal counsel for advice regarding specific circumstances.

Understanding identity theft laws usa empowers tenants and landlords alike to respond lawfully, protect their rights, and reduce long-term harm. When addressed promptly and correctly, the legal system provides meaningful tools to restore accuracy, accountability, and housing stability.