Few things create anxiety faster than a call from a debt collector—especially when the debt is something you genuinely believe you do not owe. For tenants disputing move-out charges, families arguing over utility bills, or small landlords trying to recover unpaid rent, debt collection can feel confusing, intimidating, and, at times, deeply unfair. That emotional weight is exactly why debt collection laws usa exist. These laws exist to create boundaries—clear, enforceable limits on how debts can be pursued and how people must be treated in the process.

At the federal level—often reinforced by state law—debt collection laws USA aim to balance two competing realities. On one side, creditors and landlords have a legitimate right to collect money that is lawfully owed. On the other, consumers and tenants deserve dignity, accuracy, and freedom from harassment or deception. This guide focuses on that balance, explaining what debt collectors are not allowed to do, how those rules apply in housing and rental-related situations, and where federal authority ends and state law steps in.

Throughout this article, the focus remains educational. The goal is to help renters, landlords, and consumers understand how the law works in real life, not to promise outcomes or provide individualized legal advice.

The Legal Foundation of Debt Collection in the United States

Federal Authority Under Consumer Protection Law

The backbone of debt collection laws usa is federal consumer protection legislation, most notably the Fair Debt Collection Practices Act, often referred to as the FDCPA. This federal statute applies primarily to third-party debt collectors—companies or individuals who collect debts on behalf of someone else. That includes collection agencies hired by landlords, property managers, medical providers, or credit card issuers.

Under federal law, debt collectors must follow strict standards for honesty, fairness, and respect. These standards were created after decades of documented abuse, including threats, public shaming, and relentless calling. The federal government recognized that without clear rules, the power imbalance between collectors and consumers could easily be exploited.

Many consumers are surprised to learn that the FDCPA was passed because of widespread abuse, including collectors calling late at night, contacting employers, and using false threats to force payment.

State Authority and Why It Matters

While federal law sets the baseline, state law often goes further. Many states expand protections to cover original creditors, including landlords collecting their own rent or damages. Some states impose shorter statutes of limitations, stricter communication rules, or higher penalties for misconduct.

For tenants, this distinction is crucial. A landlord collecting unpaid rent directly may not fall under every federal rule, but state law may still impose nearly identical obligations. Understanding debt collection laws usa therefore requires looking at both levels together, not in isolation.

When a Debt Becomes a Collection Matter in Housing Disputes

Common Rental Scenarios That Lead to Collection Activity

In real rental situations, most collection disputes do not start with refusal to pay. They start with confusion—like a tenant moving out, expecting their full security deposit back, only to receive a bill weeks later for “damages” they never agreed existed.

If these disputes are not resolved informally, the claimed balance can be sent to a collection agency. At that moment, debt collection laws usa become highly relevant. The legal question shifts from “Who is right?” to “How can this debt be pursued lawfully?”

Disputed Debts and the Right to Accuracy

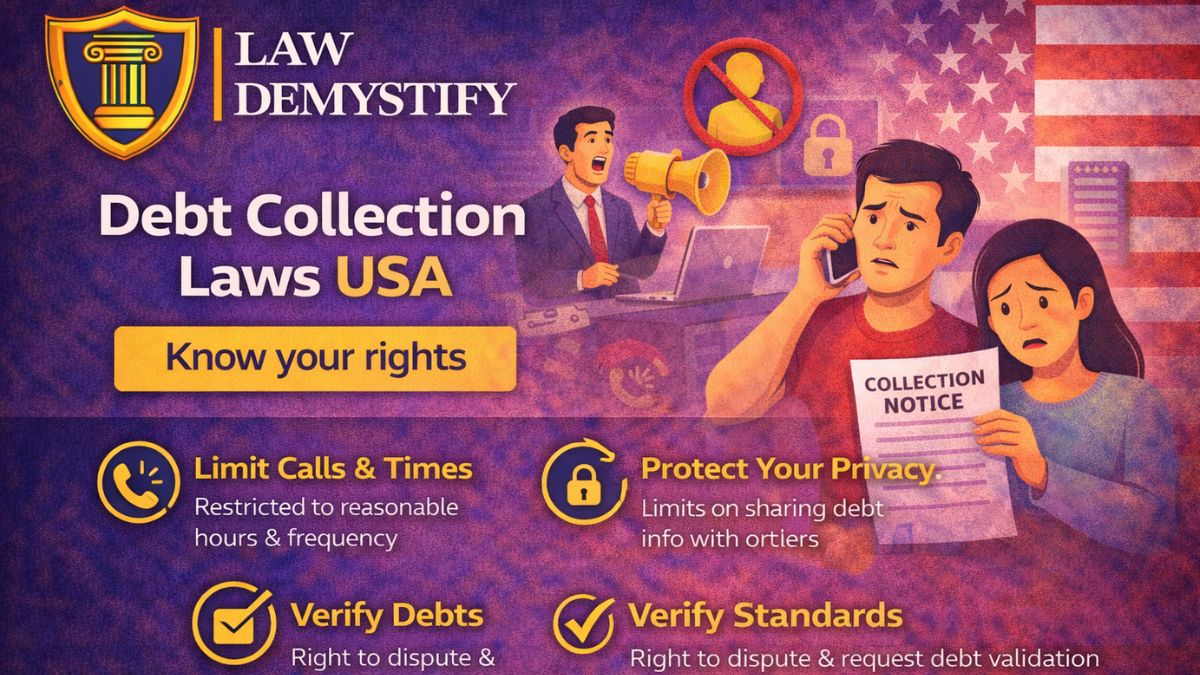

One of the most important principles in debt collection laws usa is accuracy. Collectors are prohibited from attempting to collect amounts that are not actually owed. If a tenant disputes a charge and requests validation, the collector must provide documentation supporting the claim.

In rental situations, this often means producing a lease, an itemized statement, or evidence of damages. Attempting to pressure payment without substantiation can quickly cross into illegal territory.

Debt Validation Timelines and Consumer Rights

Under federal law, consumers generally have 30 days to dispute a debt after receiving the first written notice from a debt collector. During this period, the collector must pause collection activity until proper verification is provided. Many tenants are unaware that requesting debt validation can temporarily stop calls and letters, especially in disputed rental charge situations.

Illegal Debt Collection Practices Explained Clearly

Conduct That the Law Explicitly Prohibits

The phrase illegal debt collection practices refers to actions that violate federal or state law, regardless of whether the debt itself is legitimate. These rules focus on behavior, not just outcomes. Even if money is owed, the method of collection must remain lawful.

Collectors are prohibited from using threats, deception, or abusive language. They cannot misrepresent who they are, exaggerate legal consequences, or pretend to be attorneys or government officials. These prohibitions apply equally in housing-related debts as they do with credit cards or medical bills.

Housing-Specific Examples of Illegal Conduct

Imagine a former tenant receives a call claiming that unpaid cleaning fees will result in immediate eviction or arrest. This is a clear violation. Eviction is a civil court process, not something enforced by collectors, and arrest is not a lawful consequence of consumer debt. Such behavior falls squarely under illegal debt collection practices and can trigger liability for the collector.

Fair Debt Collection Practices Act Violations in Plain English

What Constitutes a Violation

Fair debt collection practices act violations occur when collectors ignore or overstep the boundaries set by federal law. These violations are not limited to extreme abuse. Even subtle misstatements can qualify if they mislead or pressure the consumer unfairly.

For example, telling a tenant that a lawsuit is “guaranteed” when no such action has been authorized can be deceptive. Claiming that wages will be garnished without explaining that a court judgment is required may also violate the law.

Why Documentation and Language Matter

Collectors must be careful with words. Under debt collection laws usa, even the tone and phrasing of a communication can matter. Letters and calls must accurately describe the debt, identify the creditor, and explain the consumer’s right to dispute.

In rental cases, failure to correctly identify the property owner or misstating the basis for charges can create fair debt collection practices act violations, even if the underlying dispute is relatively small.

Harassment by Debt Collectors and Where the Line Is Drawn

Understanding Harassment Under the Law

Harassment by debt collectors is not just about being annoyed. It is about feeling cornered—when the phone keeps ringing, the tone gets sharper, and the pressure starts to affect your daily life.

In housing disputes, harassment often shows up when emotions are already high. A tenant facing multiple daily calls about a contested fee may feel trapped or bullied. Debt collection laws usa step in to prevent exactly this kind of pressure.

Real-World Rental Example

Consider a tenant who disputes a $500 carpet replacement charge. If a collector calls ten times a day, leaves aggressive voicemails, and contacts the tenant’s workplace, that behavior likely constitutes harassment by debt collectors. The law does not allow frequency or embarrassment to be used as a collection strategy.

What Debt Collectors Cannot Do Under Federal Law

Absolute Prohibitions That Apply Nationwide

Understanding what debt collectors cannot do is central to debt collection laws usa. These prohibitions apply regardless of the debt amount, the consumer’s financial situation, or the collector’s frustration.

Collectors cannot threaten violence, arrest, or criminal charges. They cannot publish lists of alleged debtors. They cannot seize property without a court order. They cannot continue collection efforts after receiving a written request to cease communication, except in limited circumstances.

How These Rules Affect Landlords and Property Managers

Landlords who hire collection agencies must be aware that they can be indirectly affected by violations. While the collector is typically the primary party responsible, improper practices can damage reputations, delay recovery, and complicate housing disputes. Knowing what debt collectors cannot do helps landlords choose compliant partners and avoid escalation.

Debt Collection Call Rules and Communication Limits

Time, Place, and Manner Restrictions

Debt collection call rules exist to protect consumers’ daily lives. Under federal law, collectors generally may not call before 8 a.m. or after 9 p.m. local time. They must stop calling if told that a workplace prohibits such communication.

For tenants, this matters because housing-related debts often overlap with work hours. A collector who repeatedly calls a tenant’s employer after being told to stop may be violating debt collection laws usa.

Written Requests and Their Impact

Consumers have the right to request that collectors communicate only in writing or cease communication altogether. Once such a request is received, the collector’s options narrow significantly. Continuing to call can trigger liability, even if the debt remains unresolved.

Cease Communication Requests in Practice

Consumers may also send a written request asking a debt collector to stop further communication. Once received, the collector is generally limited in how they may continue contact. Many tenants use this option when repeated calls begin to feel overwhelming or disruptive.

Federal Versus State Enforcement: Who Polices the Rules?

Federal Agencies and Oversight

At the federal level, enforcement of debt collection laws usa is handled by agencies such as the Consumer Financial Protection Bureau and the Federal Trade Commission. These agencies can investigate patterns of abuse, impose penalties, and require corrective action.

State Attorneys General and Local Remedies

States often play an even more active role, especially in housing-related disputes. Many state attorneys general have consumer protection divisions that handle complaints about rental collections. Some states allow private lawsuits with statutory damages, making enforcement more accessible to individual tenants.

State-by-State Differences That Matter in Practice

Variations in Coverage and Scope

While federal law is uniform, state laws vary widely. Some states extend debt collection rules to original creditors, including landlords collecting their own debts. Others impose stricter limits on call frequency or require additional disclosures.

For example, California’s consumer protection laws are among the most expansive, covering many practices not explicitly addressed at the federal level. Texas, by contrast, emphasizes clear notice requirements and prohibits certain deceptive practices tied to property claims.

Statutes of Limitations and Rental Debts

State law also controls how long a debt remains legally enforceable. In housing disputes, this can determine whether an old move-out charge can still be pursued. Attempting to collect a time-barred debt without proper disclosure may violate debt collection laws usa as applied through state statutes.

Lawful Collection Practices in Housing-Related Debts

What Collectors Are Allowed to Do

Not all collection activity is unlawful. Collectors may contact consumers to request payment, provide information about the debt, and explain available options. They may report accurate information to credit bureaus and pursue legal action when authorized.

The key is compliance. Lawful practices are transparent, respectful, and grounded in verifiable facts. In rental contexts, this means clearly explaining charges, providing documentation, and honoring dispute rights.

How Debt Collection Can Affect Credit Reports

In some cases, unpaid or disputed rental debts may be reported to credit bureaus. However, reporting inaccurate or unresolved debts can raise separate legal concerns. Consumers have the right to dispute incorrect credit reporting, particularly when the underlying debt is still contested or lacks proper documentation.

The Role of Professionalism

Professional conduct benefits everyone involved. Tenants are more likely to engage when treated fairly, and landlords are more likely to recover funds without prolonged conflict. Debt collection laws usa encourage this professionalism by penalizing shortcuts and abuse.

Tenant Remedies When the Law Is Violated

Recognizing a Violation

Tenants often sense when something feels wrong but may not know it is illegal. Threats, nonstop calls, or refusal to provide documentation are red flags. Understanding debt collection laws usa empowers tenants to recognize violations early.

Available Avenues for Relief

Depending on the situation, tenants may file complaints with federal or state agencies, seek damages through civil court, or use violations as leverage to resolve the underlying dispute. State laws may offer additional remedies, particularly when housing is involved.

Compliance Obligations for Businesses and Landlords

Why Compliance Is a Business Issue

For landlords and property managers, compliance is not just a legal requirement—it’s a risk management strategy. Violations can lead to fines, lawsuits, and reputational harm. Understanding debt collection laws usa helps businesses avoid costly mistakes.

Training and Oversight

Businesses that regularly deal with unpaid rent or fees should ensure that staff and third-party collectors are trained on lawful practices. Clear policies, documented procedures, and careful oversight reduce the risk of violations.

The Role of Dispute Resolution and Communication

Preventing Escalation Before Collection

Many collection disputes can be avoided through early communication. Itemized statements, clear lease language, and timely responses reduce confusion. When disputes are resolved before reaching collections, everyone benefits.

How the Law Encourages Resolution

By requiring accuracy and transparency, debt collection laws usa indirectly promote dispute resolution. Collectors who must document claims and respect disputes are more likely to engage constructively rather than aggressively.

FAQ: About Debt Collection Boundaries

Can debt collectors threaten arrest for unpaid rent or fees?

No. Threatening arrest for unpaid rent or fees is illegal. Consumer debt is a civil matter, not a criminal one, and collectors are not allowed to suggest otherwise.

Can debt collectors call at night if the tenant works late hours?

Generally, no. Federal law restricts calls before 8 a.m. and after 9 p.m. local time, regardless of work schedules, unless the consumer expressly agrees otherwise.

How can a tenant stop repeated calls from a collector?

Tenants may request in writing that communication stop or be limited to certain methods. Continuing calls after such a request may violate debt collection laws usa.

Are landlords subject to the same rules as collection agencies?

It depends on state law. Federal rules primarily target third-party collectors, but many states apply similar standards to landlords collecting their own debts.

Is it illegal to collect a debt that the tenant disputes?

Collecting is not automatically illegal, but failing to validate the debt or misrepresenting its status can violate debt collection laws usa, especially if the dispute is ignored.

Can a collector contact a tenant’s employer about a rental debt?

Contacting an employer is heavily restricted and generally prohibited unless necessary to verify location information. Using an employer to pressure payment may be unlawful.

What should a consumer do if they believe collection rules were broken?

They may document the conduct, file complaints with appropriate agencies, or explore civil remedies under federal or state law, depending on the circumstances.

For many tenants and consumers, the hardest part of debt collection is not the money—it is the uncertainty. Understanding where the law draws the line can restore a sense of control and help people respond calmly, confidently, and lawfully.